In Part 394 I laid out a scenario where two improvement teams had made improvements to different parts of a process. I then asked you "Which improvement team's project would you select if you were the CEO and why would you select it?" I told you that I would give you my answer in this posting, and I will. Remember, the purpose of Part 394 was to discuss improvements in terms of whether or not something was, in fact, an improvement and how I believe "improvements" should be evaluated. That is, what is an improvement and how should we determine if what we're doing really is considered an improvement. As a frame of refresher, the first part of this posting will be exactly the same layout as my previous posting.

I also told you that for me, the reason many improvement initiatives fail to deliver acceptable bottom line improvements is not because of the methodologies and tools themselves, it's more because of the way improvements are evaluated and savings are calculated. So what did I mean by that? I'll answer this question shortly.

I also explained that in so many companies that I have gone into, I have seen labor hours being reduced for a particular process step and the labor hours are claimed as savings when in fact they do not fall to the bottom line. I've seen wastes like too many steps to complete a product being "eliminated" but they can't seem to find these "savings" actually falling to the bottom line. I've seen celebrations of how fantastic their continuous improvement initiative is performing and yet, the savings proclaimed don't show up on the bottom line. If this sounds familiar, it's because it happens every day in virtually every company. For me, the answer to this scenario is the method used to view improvements. So the first question is, "What is the definition of improvement?" I answered this question as follows.

In order to effectively answer this question, we need to know what the company's goal is. If the company is a for-profit company, which most are, then the over-arching goal is to make money now and in the future. So if this is the goal, then how should we approach the definition of improvement? The way I look at this is, real improvements must positively impact the goal of the organization or in other words, the improvement must looked at in terms of its impact on and improvement to profit margins. Reducing hours for a particular process step does not necessarily improve profits. I then laid out the following scenario.

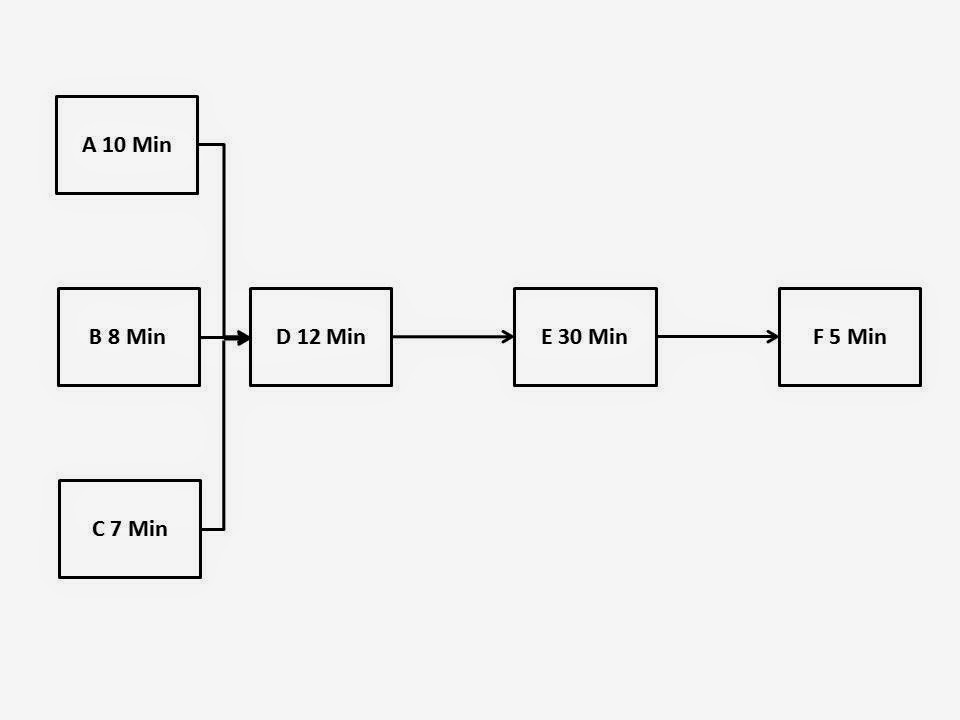

The above figure represents a company's main process for producing their product. The steps are listed as A, B, C, D, E, and F with the time it takes to produce a single unit of product. The market is strong so if this company could produce more units, it could sell them. The revenue for a single product is $500 and the raw material cost per unit is $20/part. This company has an active continuous improvement initiative in place with many on-going projects. One of the projects is in Step B, currently taking 8 minutes to complete. The team came up with an improvement idea to reduce this step from 8 minutes down to 4 four minutes, a whopping 50 % reduction in time. The team has calculated their improvement and explained that they should be able to make twice as many products that they currently make. Leadership congratulates the team and gives them all a small bonus.

Another team is working on Step E which currently takes 30 minutes to complete. This team has come up with an improvement idea that reduces the time for Step E to 26 minutes (13.4% reduction), but nobody is excited about it, so no bonus is given. Both improvement ideas cost $1,000 to implement. My question to you is, "Which improvement team's project would you select if you were the CEO and why would you select it?" I told you to remember, we're looking at which improvement contributed the most to profit improvement. OK, so let me give you my answer and an explanation as to why I answered it this way.

I think the typical first reaction by many people would be that the team that improved Step B from 8 minutes to 4 minutes, or by 50%, was the clear cut "winner." For me, it was clearly the team that improved Section E, even though their improvement only reduced their processing time by roughly 13%. So why do I say this? In order to answer this question, I first want to discuss some basic accounting concepts that I use and the system approach to continuous improvement.

On a typical profit and loss statement what is considered the top line is the revenue from sales while the bottom line in the profits. But how do we get to the bottom line? Quite simply we have to subtract things like wages, raw materials, taxes, etc. In other words, Net Profit = Sales Revenue - Materials - Operating Expenses. Return on Investment (ROI) = Net Profit/Investments. In TOC we use a form of accounting known as Throughput Accounting which uses 3 simple calculations as follows:

- Throughput (T) = Revenue - Totally Variable Costs or T = R - TVC

- Investment/Inventory ( I ) = all the money the organization invests in purchasing things it intends to sell

- Operating Expense (OE) is all the money the organization spends to convert TVC into Throughput

- NP = T - OE

- ROI = (T - OE)/I

With this form of accounting, let's take a look at the same process presented above.

This process begins with Steps A, B and C processing materials and feeding them to Step D which processes the three materials for 12 minutes and passes it on to Step E which takes 30 minutes to process before passing it to Step f which takes 5 minutes to complete and voila, you have your finished product ready for sale. There are a couple of key points to consider here. First, because Step A requires 10 minutes to complete, Step B's improvement of 4 minutes will not produce any more products because it must wait for Steps A and C to complete. If you were to run Step B to its full capacity (i.e. 1 part every 4 minutes) you would only serve to develop an excessive amount of WIP which would serve no purpose.

Now let's turn our attention to Step E. Step E limits the output of the entire process because of its long processing time of 30 minutes. Step E is, in fact, the system constraint (i.e. bottleneck) and it dictates how many parts per hour this process can produce which is 2 parts per hour, assuming no down time. So in an 8-hour shift, this process is capable of producing a total of 16 parts which translates into 16 parts/day x $500/part = $8,000 per day, assuming only 1 shift of operation. But wait, Team E reduced the processing time from 30 minutes to 26 minutes. This means that the process can now produce 18.5 parts (i.e. 480 min/shift divided by 26 min = 18.5) which means that the new revenue for an 8-hour shift increases from $8,000 to $9,250 or a net gain of $1,250 in revenue for an 8-hour shift (assuming you sold it and received money back from the customer). And since we said earlier that the market is open for more sales, we would be able to sell it and receive the additional revenue. So based upon this, Team E's improvement is by far and away superior to Team B's. But revenue is not profit, so let's look into that.

The calculation for profit is Throughput (T = Rev - TVC) minus Operating Expense (OE) or NP = T - OE. Let's say that the TVC for each part is $20 and OE for an 8 hour shift is $1,500. This means that the actual Throughput was $8,000 - $320 = $7,680. The old NP prior to the improvement was $7,680 - $1,500 = $6,180. The T after the improvement was $9,250 - (18.5 x 20 = $370) = $8,880 so the NP = $8,880 - $1,500 = $7,380 or a gain of $1,200 for an 8 hour shift. So over the course of a month, assuming 20 work days in an average month and 1 shift per day, we have increased NP by $24,000 per month or approximately $288,000 for the year.

So let's go back to the improvement team that was able to reduce Step B's processing time by 4 hours or a 50% reduction in time. While the work they did was no doubt well thought out in terms of being able to reduce time, do you see why it's so important to look at the impact of an improvement on the system (Team E's work), rather than an isolated,localed improvement (Team B's)? This is why I have integrated Lean and Six Sigma with the Theory of Constraints (i.e. TLS). Before signing off, let's take a look at Goldratt's 5 Focusing Steps.

- Step 1: Identify the System Constraint

- Step 2: Decide how to Exploit the System Constraint

- Step 3: Subordinate everything to the above decision

- Step 4: If necessary, Elevate the system constraint

- Step 5: If the constraint moves, return to Step 1, but don't let inertia create a new constraint

Bob Sproull

No comments:

Post a Comment